Is Higher Insurance Premium Worth the Cost? Discover the Hidden Risks

When considering whether a higher insurance premium is worth the cost, it's essential to evaluate what you are paying for. A higher premium often translates to better coverage, which can provide peace of mind in times of unexpected events. This can include comprehensive policies that cover not just basic damages but also liabilities and additional risks. For instance, individuals in areas prone to natural disasters might find that opting for a slightly elevated premium significantly mitigates potential out-of-pocket expenses in the event of a claim.

However, it's crucial to recognize the hidden risks associated with low-cost insurance plans. Often, these plans come with substantial deductibles or limited coverage, which could leave policyholders vulnerable when they need help the most. If you think about the costs involved, a higher premium can indeed save you from financial strain. Therefore, before making a decision, it's wise to assess not only the price tag but also the extent of the coverage to ensure that you are effectively protecting yourself against potential liabilities.

Top 5 Reasons You're Overpaying for Insurance and How to Avoid It

Many individuals unknowingly overpay for insurance due to a lack of awareness regarding the various factors that influence premiums. Reason 1: A poor credit score can significantly raise your insurance rates, as many insurers use credit scores to gauge risk. Reason 2: Failing to compare quotes from multiple providers might lead you to miss out on better deals available in the market. Reason 3: Not taking advantage of discounts, such as multi-policy or safe driver discounts, can also result in higher costs. Understanding these factors is essential to ensure you aren't paying more than necessary.

Moreover, Reason 4: outdated coverage options may leave you with unnecessary policies that inflate your premiums. Regularly reviewing your insurance needs can help eliminate this waste. Reason 5: Lastly, choosing higher deductibles without fully understanding the implications can be a misstep. To avoid overpaying for your insurance, it's crucial to evaluate your coverage, actively seek out competitive quotes, and stay updated on available discounts. By taking these proactive steps, you can secure better rates and tailor your insurance to fit your actual needs.

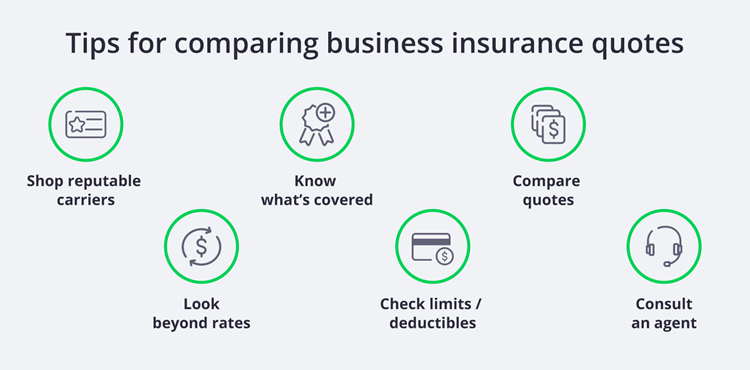

The True Cost of Insurance: Are You Paying More for Less?

The world of insurance can often feel like a maze, where navigating policies, coverage limits, and premium costs can lead you to question whether you're truly getting your money's worth. Most consumers tend to prioritize the lowest premium, believing it to be a savvy financial decision. However, this approach can be misleading. According to industry experts, the true cost of insurance extends far beyond the amount you pay monthly; it encompasses the coverage you receive, the deductibles you must meet, and the claim settlement processes. In many cases, paying a slightly higher premium can offer significantly greater peace of mind and financial protection when you need it most.

So, how can you ensure you're not paying more for less? Start by evaluating your current policy against your actual needs. Create a checklist that includes crucial factors such as coverage limits, deductibles, and exclusions. Additionally, consider seeking quotes from multiple insurers, as comparing policies can reveal hidden costs that affect the overall value. Remember, the goal is to strike a balance between affordability and comprehensive coverage, safeguarding your finances against unexpected events. In essence, being well-informed and proactive in your insurance choices can save you from the pitfalls of inadequate coverage and excessive costs.